August First Finance Chief Survey: The economy continues to recover, and the third quarter is now at a stage high.

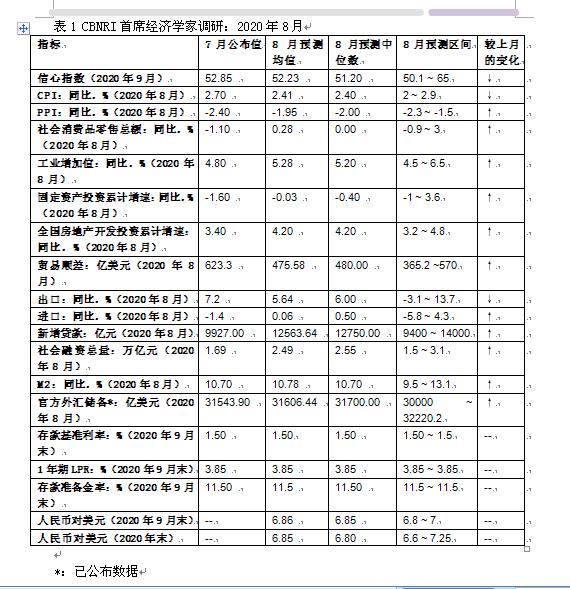

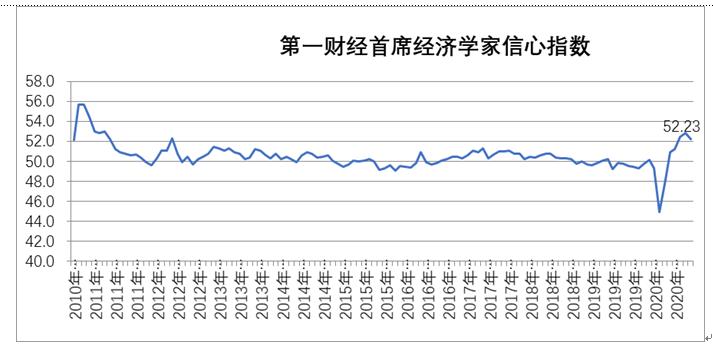

In September, 2020, the "Confidence Index of Chief Economist of CBN" was 52.23, which was lower than that of last month, but it was still at a high level in two years. This month, economists predicted that it would be higher than 50 threshold, and they thought that China’s economy would continue to improve in the coming month.

It is expected that the year-on-year growth rate of CPI will decrease in August, the year-on-year growth rate of PPI will rebound, the "scissors gap" will narrow, the year-on-year growth rate of investment and consumption will be higher than that of last month, and the trade surplus will narrow.

Economists said that with the sustained economic recovery, the proactive fiscal policy will accelerate in the future and the monetary policy will return to neutrality. In August, the year-on-year growth rate of M2 and the total amount of new loans and social financing increased, and the deposit and loan interest rates and deposit reserve ratio will remain unchanged in September.

At the same time, they believe that in the process of China’s economic transformation to a "double cycle", safeguarding people’s livelihood and optimizing the distribution system are the basis for boosting domestic demand. In the short term, specific measures can include: improving the social security system, reducing taxes and fees for small and medium-sized enterprises, and issuing consumer vouchers.

In this survey, economists once again raised their expectations for the central parity of RMB against the US dollar at the end of last month, from 6.96 at the end of last month to 6.85.

1. Confidence index: at a high point in two years.

In September, 2020, the "Confidence Index of Chief Economist of CBN" was 52.23, which was lower than that of last month, but it was still at the high point in two years. Economists who predicted this index this month all gave predictions higher than 50 threshold, and they predicted that China’s economy would continue to improve in the coming month. Among them, Ding Anhua of China Merchants Bank gave the most optimistic forecast value of 65, and Guan Qingyou of Financial Research Institute gave the lowest forecast value of this confidence index of 50.1.

Shen Jianguang of JD Finance said that China’s economy continued to recover slowly, with real estate and infrastructure investment as the main driving forces, while the recovery of total retail sales of social consumer goods was generally weak and industrial production was also facing bottlenecks. In the future, in the face of more prominent structural contradictions and complex and severe external situation, macro-policies need to pay more attention to efficiency and pertinence, push service consumption and manufacturing investment back to the right track as soon as possible, and help further economic recovery.

Li Xunlei, Zhongtai Securities, believes that the short-term improvement of production is mainly supported by real estate and infrastructure, and infrastructure comes from policy efforts, while real estate is more concentrated release of accumulated investment during the epidemic, which is difficult to sustain. After the backlog of demand and investment release process is over, the economy may gradually tend to decline. In addition to the real estate factor, the local debt supervision makes the generalized finance limited, the epidemic situation repeatedly restricts demand, and the global weak recovery restricts external demand, all of which mean that China’s economy is facing a situation of going up first and then down.

Second, prices: CPI decreased year-on-year in August, while PPI increased year-on-year.

The survey results show that the average forecast of CPI growth rate by economists in August is 2.41%, which is 0.29 percentage points lower than the July value (2.7%) published by the Bureau of Statistics. Among the 25 economists who participated in the survey, KPMG Kang Yong gave the maximum forecast value of 2.9%, while the minimum value of 2% came from Ding Anhua of China Merchants Bank.

The predicted average year-on-year growth rate of PPI in August is -1.95%, which is higher than the last month’s value (-2.4%) announced by the Bureau of Statistics. Among them, the highest predicted value -1.5% comes from Guan Qingyou of the Financial Research Institute, and the lowest value -2.3% comes from Zhu Baoliang of the National Information Center.

Changjiang securities Wu Ge said that in terms of price, the "scissors gap" situation of lower CPI and higher PPI will continue. In terms of industrial products, with the gradual recovery of global demand, the high level of international crude oil inventories has dropped. The centralized landing of domestic special bonds and other funds is expected to help the demand for "Golden September, Silver and Ten" steel to turn prosperous, and PPI deflation will be further alleviated. In terms of consumer prices, the start of the school season has helped stabilize the core inflation rates such as education, housing and services. However, under the extremely high base of the impact of swine fever in the same period last year, the overall inflation center will continue to decline in the future, and even the possibility of zero growth at the end of the year will not be ruled out.

— — — — — — — — — — — — — — — — — — —

The Best Forecast in July Economists’ August Forecast (CPI):

Ding Shuang: 2.4%

Angkor: 2.2%

Li Wenlong: 2.4%

Lu Ting: 2.1%

Shen Jianguang: 2.2%

The Best Forecast in July Economists’ August Forecast (PPI):

Li Xunlei: -2.2%

Jiang Chao: -2.1%

— — — — — — — — — — — — — — — — — — —

III. Total retail sales of social consumer goods: the average growth rate rose to 0.28% in August.

According to the statistics bureau, the total retail sales of consumer goods in July increased by -1.1% year-on-year, and economists expect the data in August to rebound to 0.28%. Among them, the maximum forecast value of 3% comes from Tang Jianwei of Bank of Communications, and the minimum forecast value of -0.9% is given by Li Xunlei of Zhongtai Securities.

Wang Han of Industrial Securities said that consumption may gradually pick up. Affected by the normalization of epidemic prevention and control, the recovery of consumption may still be slow; But at the same time, economic activity rebounded, supporting consumption to further pick up. It is expected that the total retail sales of consumer goods will continue to rise year-on-year, and the growth rate may turn positive.

IV. Industrial added value: the average growth rate increased by 0.48 percentage points.

The survey results show that the forecast average year-on-year growth rate of industrial added value in August is 5.28%, which is 0.48 percentage points higher than the July value (4.8%) announced by the Bureau of Statistics. Among them, KPMG Kang Yong gave the minimum value of 4.5%, and Haitong Securities Jiang Chao gave the maximum value of 6.5%.

Huang Jianhui, Minsheng Bank, said that from the leading indicators, the production index in the official manufacturing PMI in August was 53.5%, down 0.5 percentage point from the previous month, ending the recovery momentum for two consecutive months. The Bureau of Statistics believes that the production in some areas has declined mainly due to the flood disaster. However, in August, Caixin PMI’s production index was the highest since February 2011, accelerating its expansion for two consecutive months. According to the survey sample enterprises, the manufacturing industry continued to recover from the COVID-19 outbreak at the beginning of the year, and the customer demand showed signs of strengthening. Judging from the high-frequency indicators, the overall production of the enterprise is still being repaired, and it has approached or exceeded the normal year level. The average operating rate of blast furnace in August was 71.1%, which was higher than 70.2% in last month and 68.2% in the same period last year. The operating rate of semi-steel tires of automobile tires is 70%, which is also higher than that of last month and the same period of last year, and has rebounded to the highest level this year. On August 17, the press conference of the National Development and Reform Commission said that the national average daily power generation and unified power load hit record highs in August. Considering that the year-on-year growth rate of industrial added value in the same period last year was the lowest in 2019, it is expected that the industrial added value will rebound to 5.2% in August.

V. Growth rate of investment in fixed assets: the average value increased by 1.57 percentage points.

Economists predict that the average growth rate of fixed asset investment in August is -0.03%, which is 1.57 percentage points higher than the July value (-1.6%) announced by the Bureau of Statistics. Among them, China Merchants Bank Ding Anhua gave the highest value of 3.6%, and KPMG Kang Yong gave the lowest value of -1%.

Lu political commissar of Industrial Bank said that in August, with the middle and lower reaches of the Yangtze River out of the long rainy season, infrastructure and real estate projects also accelerated. In terms of high-frequency data, since August, the prices of rebar and cement have re-entered the upward channel, and the industry inventory has improved significantly. Judging from the operating rate of petroleum asphalt plant, the operating rate of petroleum asphalt plant rose sharply to 58.0% in August, the highest since 2019. Infrastructure investment is expected to continue to rise. In terms of manufacturing investment, the current demand side has improved, and the follow-up is expected to continue to repair.

— — — — — — — — — — — — — — — — — — —

The best forecast in July Economists’ August forecast (cumulative growth rate of fixed asset investment):

Ding Shuang: -0.5%

Zhu Haibin: -0.2%

— — — — — — — — — — — — — — — — — — —

VI. Investment in real estate development: the average growth rate is 4.2%.

The survey results show that the predicted average growth rate of real estate development investment in August is 4.2%, which is higher than the July value (3.4%) announced by the Bureau of Statistics. Among the economists who participated in the survey, Jiang Chao of Haitong Securities gave the highest value of 4.8%, and Guan Qingyou of Financial Research Institute gave the lowest value of 3.2%.

Ding Anhua of China Merchants Bank believes that overall, the real estate investment data in July still shows the strong resilience of the real estate industry, and the future real estate boom is expected to continue. However, as the Politburo meeting at the end of July reiterated that housing should not be speculated, and the central bank’s monetary policy implementation report in the second quarter mentioned that real estate should not be used as a short-term means to stimulate the economy, the regulation policies of hot cities in the future are still expected to continue to be introduced. Under this background, it is unlikely that the growth rate of real estate investment will continue to rise in a single month.

— — — — — — — — — — — — — — — — — — —

Best Forecast in July Economist’s August forecast (cumulative growth rate of real estate development investment):

Jiang Chao: 4.8%

— — — — — — — — — — — — — — — — — — —

VII. Foreign Trade: The trade surplus in August narrowed compared with last month.

Economists predict that the trade data in August will narrow from the surplus of $62.33 billion last month to $47.558 billion, the export data will be lower than last month, and it will drop from the published data last month (7.2%) to 5.64%. The import value is expected to be 0.06%, which is higher than the July data (the official published value is -1.4%).

Standard Chartered Bank Ding Shuang expects strong export and import performance in August. This month, the official PMI new export order index increased by 0.7 percentage point to 49.1, the highest since January. In August, the initial PMI of the United States rose, indicating that external demand continued to improve, while the euro zone changed little. The export support measures taken by China also played a positive role in improving exports. It is estimated that the year-on-year growth of exports in August has accelerated to 6.0%, and exports in the third quarter have greatly improved compared with the second quarter. The year-on-year growth rate of imports in August accelerated to 2.5% after 1.4% in July. International oil prices rose in August, and China may have increased its imports of energy and agricultural products to the United States to meet the requirements of the first phase of Sino-US trade negotiations. China’s trade surplus in August is expected to narrow from $62.3 billion in July to $43.2 billion.

Eight, new loans: the average rose to 1,256.364 billion yuan.

Economists predict that new loans in August will increase from 992.7 billion yuan last month to 1,256.364 billion yuan.

Xie Yaxuan, China Merchants Securities, said that since August, monetary policy has gradually stabilized and the growth rate of government debt has also started to pick up significantly. In terms of commodity prices, the CRB spot composite index has continued to rise since the end of June, or more from the recovery of external demand and the weakness of the US dollar. On the whole, according to a series of regulatory targets announced by the government and such a low excess reserve ratio in July, there is no room for further increase in the growth rate of follow-up liabilities of the two private entities, namely households and non-financial enterprises. Although the government still has a large room for table expansion, it is still difficult to determine when and how much it will be applied. He predicted that the financial data in August (M2 year-on-year, loan balance year-on-year, social financing balance year-on-year) may remain basically stable compared with that in July, and even if there is an increase in the follow-up, the space is very narrow.

IX. Total social financing: The average value is estimated to be 2.49 trillion yuan.

The survey results show that the average forecast of total social financing in August is 2.49 trillion yuan, which is higher than the data released by the central bank in July (1.69 trillion yuan).

Jiang Chao of Haitong Securities said that in July, the social financing increased by 1.69 trillion yuan, an increase of 406.8 billion yuan year-on-year, of which RMB loans and undiscounted bank acceptance bills were the main contributions. Since the beginning of this year, the interest rate of residents’ mortgage has dropped slightly, which has helped the growth rate of residents’ medium and long-term loans to stop falling and rebound. As the epidemic subsides, the replenishment cycle has been restarted, which is expected to support the growth rate of medium and long-term loans of enterprises to continue to rise. Coupled with the acceleration of government bond issuance, it is expected that the growth rate of social financing and broad money M2 will continue to pick up. In August, the scale of new credit is expected to reach 1.2 trillion yuan, and the new social financing will reach 2.6 trillion yuan, with an M2 growth rate of 10.9%.

X M2: The average growth rate is 10.78%.

Economists expect the year-on-year growth rate of M2 to be 10.78% in August, higher than the data released last month (10.7%). Among them, changjiang securities Angkor gave the maximum value of 13.1%, and Guan Qingyou of the Financial Research Institute gave the minimum value of 9.8%.

Lian Ping of Zhixin Investment believes that in terms of money supply, the year-on-year growth rates of M0, M1 and M2 in July were 9.9%, 6.9% and 10.7%, respectively, which were 0.4, 0.4 and -0.4 percentage points higher than the previous month. The currency multiplier continued to hit a new high of 7.15. In August, although the central bank increased the amount of MLF (medium-term lending facility) and resumed the 14-day open market reverse repurchase operation, the increase in the number of bond issuance still caused the liquidity in the interbank market to increase significantly. In late August, R007 increased by about 40 basis points from the beginning of the month to 2.50%. At the same time, the stock market trading is still active, which will continue to incite the activation of RMB deposits, further narrowing the "M2-M1" scissors gap. He predicted that the year-on-year growth rate of M2 will drop slightly by 0.1 percentage point to 10.6% in August.

XI. Interest rate-deposit reserve ratio: the one-year LPR interest rate remains unchanged.

The 18 chief economists who predicted the benchmark deposit interest rate all predicted that the benchmark deposit interest rate would not change in the next month. At the same time, they do not expect the deposit reserve ratio to be lowered in September.

Changjiang securities Wu Ge said that in terms of currency, the recent pressure drop of structured deposits and marginal changes in housing financing seem to have reflected the signal of weakening aggregate easing. At present, the medium and long-term loans of enterprises are still bright, but the external demand has shown signs of stabilization. After the centralized issuance of government bonds, the growth rate of monetary social financing is expected to usher in an inflection point. In view of the fact that China’s interbank interest rate is close to the pre-epidemic level, and the nominal GDP recovery rate may slow down in the fourth quarter, it is difficult for the interbank market interest rate to have an obvious upward trend in the past one or two quarters, and the shock characteristics may be more obvious.

XII. Exchange rate: The average value in September remained stable, and the expectation of the exchange rate at the end of the year was raised.

Economists expect that the RMB against the US dollar will remain stable at the end of September compared with the data at the end of August (the central parity of RMB against the US dollar was 6.8605 on August 31), and the expectation for the central parity of RMB against the US dollar at the end of the year will be raised from 6.96 at the end of last month to 6.85.

Tang Jianwei, Bank of Communications, said that since August, due to the weak trend of the US dollar index and the fundamentals of China’s economic recovery, the RMB exchange rate has continued to appreciate. As of August 25th, the central parity of RMB against the US dollar was reported at around 6.92, which was about 1% higher than that at the end of last month. The FOB price of RMB approached 6.90, which was about 1.2% higher than the end of last month. Looking forward to September, the peak number of newly diagnosed people in the United States has declined. In August, the manufacturing PMI reached the highest level since January 2019, while the manufacturing PMI in the euro zone was less than expected, which will support the continued weak US dollar index. However, in contrast, China’s economic performance is obviously relatively leading, and the stock and bond market is expected to continue the net inflow of funds under the large spread between China and foreign countries, and the RMB exchange rate has strong fundamental support. Recently, the leaders of Sino-US trade negotiations made a phone call and agreed to create conditions and atmosphere to continue to promote the implementation of the first-phase economic and trade agreement between China and the United States. It is reported that the exchanges between the two sides in agriculture and finance are relatively smooth. Therefore, it is expected that the RMB exchange rate will slightly break through the 6.9 mark. However, with the approach of the US election, Sino-US friction may still pose a phased depreciation pressure on the RMB exchange rate. It is expected that the RMB exchange rate may fluctuate strongly and the probability of a sharp appreciation is small.

XIII. Official foreign exchange reserves: The average at the end of August was $3,160.644 billion.

At the end of July, the balance of China’s foreign exchange reserves was US$ 3,154.4 billion, an increase of US$ 42.1 billion compared with the end of June, with a positive growth for four consecutive months. Economists expect this figure to increase to $3,160.6 billion by the end of August.

Huang Jianhui, Minsheng Bank, said that from the perspective of exchange rate factors, the US dollar index declined slightly in August, while the Japanese yen, euro and pound appreciated against the US dollar, and the valuation of the foreign exchange reserves denominated in non-US dollar currencies increased after being converted into US dollars. From the perspective of bond prices, the bond yields of major countries have risen, which has led to a decline in the bond prices held by China and a decrease in the book value of foreign exchange reserves. Considering the effect of exchange rate conversion and asset price change, the change of valuation makes the scale of foreign exchange reserves decrease. From the perspective of cross-border capital flows, the domestic economic situation has gradually improved recently, RMB assets have been favored by international investors, and RMB bonds held by overseas institutions have shown a sustained growth trend. From August 1 to 28, the net inflow of funds from the north was 6 billion yuan, which supported foreign exchange reserves. From the perspective of foreign trade, the manufacturing PMI of major overseas economies such as the United States, Japan and Britain continued to improve in August, and the PMI index of new export orders in China rebounded by 0.7 percentage points to 49.1%, which was basically close to the pre-epidemic level. The improvement of external demand is conducive to export growth, thus playing a positive role in the increase of foreign exchange reserves.

XIV. Policy Outlook: The proactive fiscal policy will be accelerated and the monetary policy will return to neutrality.

For example, Guan Qingyou of the Financial Research Institute believes that the economy will continue to recover weakly, especially the infrastructure will continue to strengthen, and there will be a staged high point in the third quarter. The main tone of monetary policy in the future is loose, but it will be marginally tightened, and it is difficult to reproduce the comprehensive RRR cut and interest rate cut in the short term.

Jiang Chao of Haitong Securities predicted that this round of economic recovery in China is expected to last until the first half of 2021. He predicted that the GDP growth rate is expected to rise to around 6% in the second half of the year. By the first half of 2021, due to the low base, the GDP growth rate may exceed 7% in the short term, and it may fall back to around 6% in the second half of next year. At the same time, with the upward growth of currency, inflation in China will also bottom out again. He predicted that the proactive fiscal policy will accelerate in the future and the monetary policy will return to neutrality.

In this survey, economists all believe that in the process of China’s economic transformation to a "double cycle", safeguarding people’s livelihood and optimizing the distribution system are the basis for boosting domestic demand. In the short term, specific measures can include: improving the social security system, reducing taxes and fees for small and medium-sized enterprises, and issuing consumer vouchers.

Shen Jianguang of JD Finance said that measures such as issuing consumer vouchers, relaxing consumption restrictions and insisting on "staying in the house and not speculating" can be taken to promote consumption recovery, especially the service consumption that has been hit harder by the epidemic. In the medium and long term, vigorously developing the digital economy, accelerating the construction of new urbanization, and promoting the reform of fiscal, taxation and land markets will all help to release the potential of the domestic market, improve the efficiency of economic operation, and then smooth the "great domestic cycle."

Zhu Baoliang of the National Information Center believes that boosting domestic demand can start from the following three points: First, promote the reform of factor markets, improve the efficiency of factor allocation, and enhance the potential growth capacity. The second is to solve the initial distribution problem through the improvement of the factor market. Improve the social security system, collect real estate tax and capital gains tax to solve the problem of income redistribution. Third, short-term fiscal expenditure is inclined to expand consumption. Expand consumption through coupons, work-for-relief and subsidies for replacement of automobile and household appliances.

List of 25 economists in this issue of "Monthly Survey of Chief Economists of CBN" (in alphabetical order):

Cheng Shi: Head, Managing Director and Chief Economist of ICBC International Research Department.

Ding Anhua: Chief Economist of China Merchants Bank

Ding Shuang: Chief Economist, Standard Chartered Bank Greater China

Guan Qingyou: If he is the president of the Financial Research Institute.

Kang Yong: Chief Economist of KPMG China.

Huang Jianhui: Dean of China Minsheng Bank Research Institute.

Jiang Chao: Chief Economist of Haitong Securities.

Li Wenlong: Chief Economist, Huanya Digital Economy Research Institute.

Li Xunlei: Chief economist of Zhongtai Securities.

Lian Ping: Dean of Zhixin Investment Research Institute

Lu Ting: Chief Economist, Nomura Securities China

Tang Jianwei: Chief researcher of Bank of Communications

Political commissar Lu: Chief economist of Industrial Bank.

Shen Jianguang: Vice President of JD.COM Group and Chief Economist of JD.COM Digital Technology.

Wang Tao: Head of Asian Economic Research and Chief China Economist at UBS.

Wang Han: Chief Economist of Industrial Securities

Wen Bin: Chief Researcher of Minsheng Bank

Wu Ge: Chief economist of changjiang securities.

Xie Yaxuan: Chief Macro Analyst of China Merchants Securities

Xu Sitao: Chief Economist of Deloitte China.

Zheng Houcheng: Director of Securities Research Institute of Yingda University

Zhou Hao: Chief Economist, China, Commerzbank.

Zhou Xue: Asian economist of Mizuho Securities.

Zhu Haibin: Chief economist of JPMorgan Chase.

Zhu Baoliang: Director and Chief Economist of Economic Forecasting Department of National Information Center.